The Summer Slowdown Is Real. Now It’s Time to Get Scrappy.

The numbers don’t lie. After a relatively strong Q1, many DTC brands on Shopify are watching sales stall out this summer. But is it just another sluggish July—or the start of a broader reset?

From rising tariffs and margin pressure to consumer confidence cratering, the mid-2025 picture is muddier than most expected. And while some operators are still growing, others are quietly pulling back, shelving product launches, or shutting down entirely.

Here’s what the data is telling us—and what to do about it.

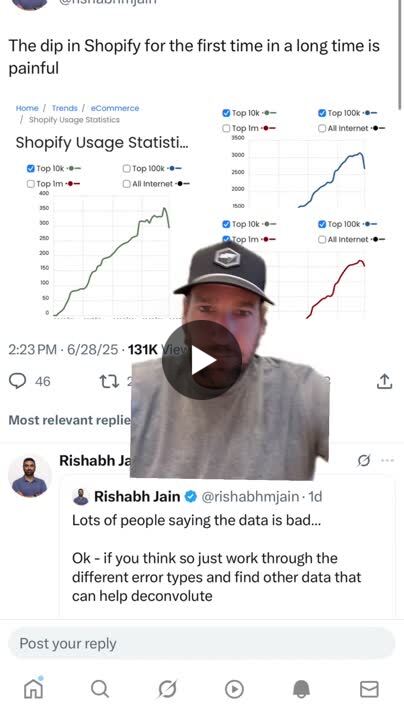

Shopify Store Revenue Down 9% in June

Data from Varos, pulled from thousands of Shopify stores, shows DTC revenue dropped ~9% year-over-year in June 2025—a sharp deceleration after a steady spring (LinkedIn).

The pullback isn’t across the board. Categories like home goods, casual apparel, and accessories are dragging, while travel-adjacent and essential products are holding up.

- Allbirds, once a DTC darling, reported an 18% revenue decline in Q1 2025 (Allbirds IR).

- Finaloop CEO Leo Namdar noted that “even 7-figure brands are closing shop,” citing a wave of Chapter 11 filings among mid-sized players (LinkedIn).

- Mastercard’s June SpendingPulse showed retail spending rising—but only because of inflation, not volume (KPMG).

Many brands expected a soft July, but not like this.

Consumer Confidence Is in the Gutter

It’s not just operators feeling it. Consumers are nervous—and acting like it.

- The University of Michigan’s sentiment index dropped to 60.5 in June, its lowest level since 2023 (Trading Economics).

- KPMG’s July survey found 40% of U.S. households reporting lower income than a year ago, with spending down in 15 of 17 discretionary categories (KPMG).

- Yet 58% still plan summer travel, cutting back elsewhere to afford it.

“Shoppers aren’t just belt-tightening—they’re rethinking value altogether,” the KPMG team wrote. Think discount codes, bundling, and yes—thrift shopping (which is up ~2% YoY).

Most telling? 70% of U.S. consumers believe a recession is coming within 12 months (KPMG). Whether it materializes or not, that perception is already shaping their behavior.

Acquisition Is Getting Pricier—And Less Efficient

Advertising isn't helping.

- Meta ad CPMs hit $12.74 in June, continuing a steady rise over 2024 (Shopify).

- Despite this, DTC ad spend rose 8% year-over-year, but return on ad spend (ROAS) declined across most sectors (The DTC Times).

As Ramp CEO Eric Glyman put it, “61% of retail brands cut spend in April, but scrappy operators are spending more—because they have to.”

Meanwhile, discounting is back in fashion. The average sitewide offer climbed to 10% off, up from ~6% in prior years. It’s a tough cocktail: rising CAC, soft conversion, deeper promo pressure.

Tariffs, Inflation, and the Margin Squeeze

If ad costs weren’t enough, supply chain pressure is building again:

- In June, the U.S. doubled tariffs on steel and aluminum imports, impacting everything from water bottles to furniture (Zonos).

- Imports from China still face 20–30% duties, and low-value de minimis exemptions have been wiped out for many categories.

Brands that manufacture or source abroad are feeling it.

“We’re treating tariffs and ad CPM hikes as the bootcamp we maybe needed,” one DTC CEO told The DTC Times. “If we can survive this, we’ll come out stronger.”

Labor isn’t helping either. 3PLs, support staff, and even payment processors have all gotten more expensive in 2025. Shopify merchants—especially those in low-margin verticals—are caught in the vise.

So, Is This the New Normal?

It might be.

PYMNTS reported that U.S. ecommerce growth slowed to 6.1% YoY in Q2, the weakest pace in over two years. Their summary: “The post-pandemic splurges are behind us” (PYMNTS).

But “slowdown” doesn’t mean “shutdown.”

The single most important business metric… ‘Will people come back and buy it?’ Acquisition will always get more expensive… If you can’t get them to come back, you are just a transaction machine.”

—Sean Frank, Ridge Wallet (LinkedIn)

Some brands are winning through:

- Operational discipline

- Strong repeat purchase rates

- Diversification into wholesale and marketplaces (Q1 wholesale growth led for sub-$50M brands)

Others are retreating and focusing on retention—where tools like LiveRecover are increasingly part of the SMS-based re-engagement playbook. Real people following up > abandoned carts.

Strategic Playbook for Q3-Q4

Here’s how the savviest brands are navigating the summer malaise:

- Trim the fat: Cut underperforming SKUs. Renegotiate supplier terms.

- Protect your margin: Push AOV, optimize bundles, hold the line on discounting where possible.

- Refocus ad spend: Prioritize ROAS-positive channels and segment audiences tighter.

- Lean on your list: LTV is the name of the game. If you're not maximizing post-purchase engagement, you're leaving money on the table.

- Brace for Q4 early: Inventory planning will be tricky with demand uncertainty and tariff exposure. Forecast cautiously.

The Bottom Line

Yes, this summer’s tough. But this isn’t a collapse—it’s a compression. And compression creates clarity.

If you’re profitable, build deeper moats. If you're not, simplify, stabilize, and survive. Fall and Q4 will favor brands that made hard decisions in July.

Subscribe for weekly DTC insights.