In 2025, DTC operators aren’t bragging about CAC (Customer Acquisition Cost) anymore. They’re talking TER, MER, and payback windows.

With funding tightening and e-commerce growth cooling, Shopify brands are being held to a new standard: capital efficiency. You’re not judged on how fast you grow—but how well you do it.

“If you’re starting in ecom, you better be thinking about profit from DAY ONE. Not some mythical LTV that’ll save you in year three.” — Operators

Welcome to the era of smarter, leaner metrics.

TER: The $1-to-Revenue Test Investors Are Obsessed With

Traction Efficiency Ratio (TER) = LTM net revenue ÷ total equity raised.

Coined by investor Kiva Dickinson, TER tells you how much real revenue a brand has generated per dollar of outside capital. According to Dickinson:

A TER above 2.0x is strong for brands doing $1M–$15M in revenue

The best consumer startups hit 5–10x TER at Series A

A TER under 1.0? That’s a red flag—it means you’ve raised more than you’ve earned

TER is the BS detector for CPG investing. It bakes in growth, margin, and burn discipline into one number. And because it reflects capital efficiency, it tells investors how much future dilution may—or may not—be needed to hit scale.

Smart operators flex spend when MER climbs and tighten when it dips. It’s not about perfection—it’s about balance.

LTV:CAC and Payback: The Speed of Profit Matters

LTV:CAC has long been a DTC staple. But now, it’s not just about the ratio—it’s about how fast you earn it back.

A 3:1 LTV:CAC ratio is still a baseline

A CAC payback window under 6 months is now considered excellent (Saras Analytics)

Anything over 12 months? Investors are asking hard questions

You can’t rely on hypothetical LTV years out. You need real retention and repeat revenue to prove it. Vuori, for example, hit a ~4:1 LTV:CAC and remained profitable while scaling (ClickZ).

“Not some mythical LTV that’ll save you in year three.” — Ridge Wallet CEO via Operators

This shift is forcing brands to rethink how they recover CAC—starting with first-order profitability. One of the most overlooked leaks in the funnel? Abandoned checkouts.

That’s where tools like LiveRecover earn their keep.

Instead of retargeting these customers through another paid channel, LiveRecover deploys real humans to follow up via SMS—turning what would’ve been lost revenue into a recovered order with no additional CAC. It’s not just a nice-to-have recovery tool—it’s a first-order margin booster, a payback window shortener, and a rare example of post-click conversion support that actually improves financial metrics your CFO (and your board) cares about.

What Does “Good” Look Like in 2025?

Benchmarks:

Metric

Healthy Range

Notes

TER

>2.0x

Top brands hit 5–10x

MER

1.5x–4.0x

3x is solid; <2x = dangerous

LTV:CAC

≥3:1

4–5:1 = elite

Payback

<6 months

<3 months = rocket fuel

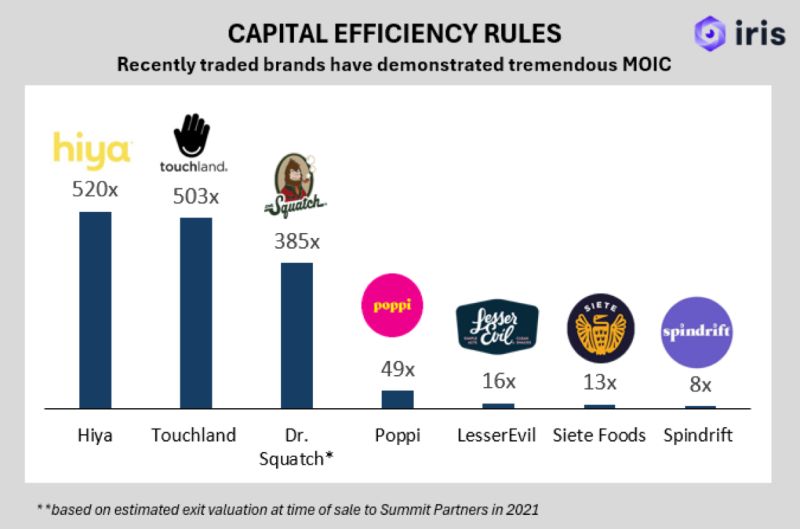

High-efficiency brands—like Native Deodorant ($30M on $500K raised, per Codie Sanchez)—prove that you don’t need mega funding to scale. Just margins, scrappiness, and a sharp eye on unit economics.

Paid social efficiency rebounded in Q1 2026: clicks up 42%, CPC down 22%, Instagram Reels leading the arbitrage. The operator's playbook for where to allocate.

The Inflection Point: Repeat Buyers Are Now Your Growth Engine

If you're still riding the acquisition hamster wheel, it's time to pivot. Nearly 60% of revenue for DTC brands now stems from repeat customers (Metrilo). Forget chasing every new customer like it's 2015. The real winners are those converting one-time buyers into loyal patrons who return and spend more over time. The numbers paint a clear picture: retention isn't just a strategy; it's survival.

Why Retention Is Crushing Acquisition